30 October 2018

On 29 October 2018 Philip Hammond delivered his latest body blow to the UK’s buy to let industry, seemingly aimed at the smaller scale end of that industry.

The change he announced impacts the Capital Gains Tax position where a property which was formerly the landlord’s home but is now rented out to tenants gets sold.

Currently the gain on such properties benefits from two important tax reliefs:

- PPR (Principal Private Residence) relief – this shelters from tax the proportion of the gain on sale relating to the period when the property was the owner’s home. Importantly it treats the last 18 months of ownership as if it were so occupied regardless of whether or not it actually was.

- Letting relief – applicable only if PPR is also available in relation to the property, this relief shelters a proportion of the gain relating to the period when the property was rented out, that proportion being capped at the lower of either the PPR relief or £40,000 if one of those is lower than the amount of gain referable to the let period.

Effective for property sales taking place on or after 6 April 2020 both of these reliefs will be lessened.

The final period exemption for PPR will halve from 18 months to nine months.

More dramatically the letting relief will be restricted to only apply to situations where the tenant and landlord are in some form of joint occupation and not to the more common scenario where the landlord has moved out. Given that having a lodger does not impede PPR relief under current rules it could be that letting relief becomes almost obsolete by virtue of this change.

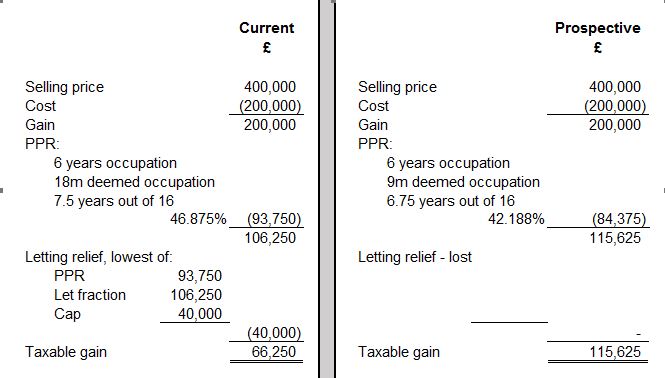

By way of illustration consider a house bought January 2005 for £200,000 and occupied by the owner until December 2010, rented out until December 2021 and then sold for £400,000:

With headline tax rates at 28% for residential property gains that could mean an increased tax charge of nearly £14,000 in this relatively normal looking scenario.

If you are currently renting out your former home and are considering a disposal of the property within the next five years or so it would be sensible to seek advice as to how these prospective changes will impact your tax position, as well as to understand any other tax planning opportunities available to you and the way in which other changes to the taxation of rental properties impact you.

If you think any of the above may be applicable to you, please do not hesitate to contact me or your local UHY specialist to discuss your options.

Alternatively, fill out our contact form here.