Publications that covered this story include: City AM and Bloomberg on 15 April 2019.

- Almost £1.1bn raised on junior market so far in 2019…

- … but IPOs slide to lowest level in a decade

Despite Brexit worries, there was still more money raised on London’s AIM market in the first quarter of 2019 than on eight of its European growth market rivals combined.

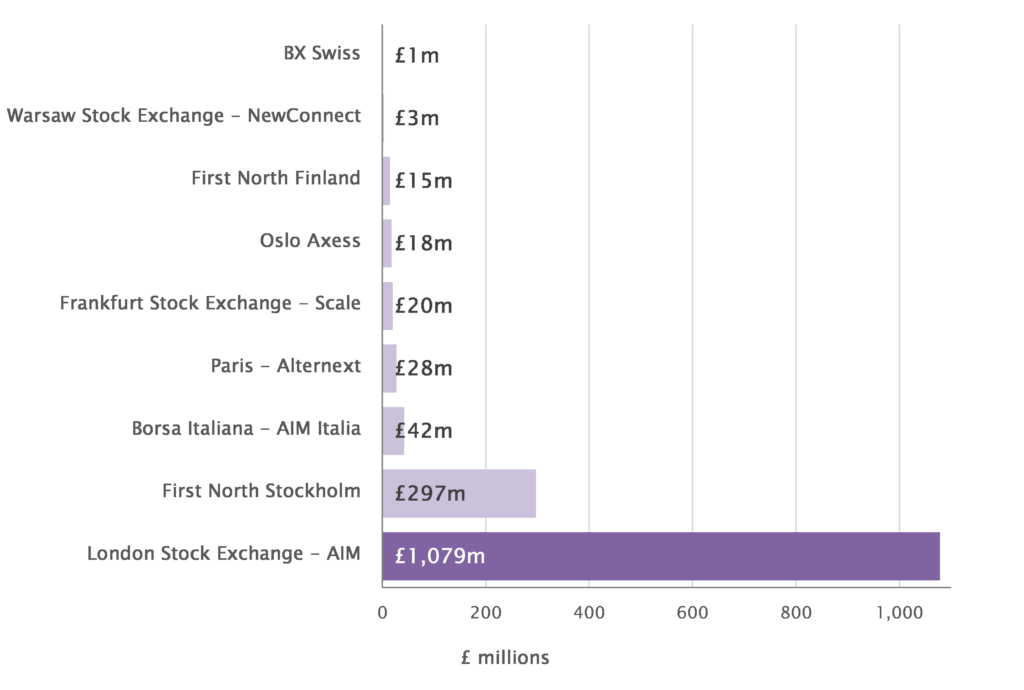

AIM companies raised almost £1.1 billion in 106 fundraises* in the first three months of this year, compared with £424 million raised in 41 fundraises on eight other junior markets in Europe**. This includes IPOs and secondary fundraises such as rights issues.

AIM’s closest rival in fundraising so far in 2019, First North Stockholm, saw £297 million of funds raised in the first quarter – just 28% of AIM’s total for the quarter (see graph below).

The firm says that continued successful fundraising on AIM shows that the market is able to weather the storm of political uncertainty, and remain Europe’s leading market for growth companies.

AIM’s largest secondary fundraises in the first quarter of the year were:

- £160m raised by identity data provider GB Group

- £126m raised by Greencoat Renewables, the renewable energy operator

- £107m raised by insurance business Randall & Quilter

Laurence Sacker, managing partner in our London office, comments: “Even with worries over Brexit, AIM is proving that it is still Europe’s best exchange for growth company fundraising.”

“AIM is a much leaner and heathier market now than it was a decade ago. A combination of tough economic conditions and more robust market requirements have led to weaker companies leaving the market, and better-run companies surviving and growing.”

AIM fundraising in Q1 more than treble that of closest European rival

Brexit impact slows IPOs on AIM

Brexit has had a negative impact on IPOs on AIM in the first quarter of 2019. The junior market saw just one IPO in the first three months of the year, with pharmaceutical data analytics provider Diaceutics PLC raising £20.75m when it floated in March. This represents the lowest IPO activity since Q1 2009 and lowest volume since Q1 2013.

AIM has followed the trend seen around the globe in the first quarter of the year, as the late-2018 fall in equities impacted IPO levels worldwide. Data from Refinitiv shows proceeds from Eurozone IPOs fell 99% in Q1 of 2019 compared to the same quarter in 2018, while US and China IPOs raised half of their Q1 2018 totals.

Q1 of 2018 saw nine AIM IPOs raise £216m. Five years ago in Q1 of 2014, 17 AIM IPOs raised almost £1.3bn.

Signs for the second quarter of 2019 are more positive, however, with Loungers PLC, which operates the Lounge and Cosy Club brands of café bars, reported to be aiming to raise £250m when it floats in April.

Laurence Sacker: “While investors in growth businesses are still comfortable in taking part in AIM’s secondary fundraises, Brexit seems to have led to a wait-and-see approach among companies considering floats.”

“AIM has thrived through a number of downturns, meaning most investors are not ‘spooked’ by the potential effects of Brexit. They can take a longer view and be confident that the market will bounce back.”

* First North Stockholm, Borsa Italiana-AIM Italia, Paris – Alternext, Frankfurt Stock Exchange-Scale, Oslo Axess, First North Finland, Warsaw Stock Exchange-New Connect MTF, BX Swiss AG