One of the key success factors of these projects is to be able to dive into the performance of a dealership and call out what is unusual, exceptionally well-managed or which could be a post-acquisition upside for the acquiring party.

Often, to drill into the data supplied (which is usually plentiful – dealers do love data!) we use several calculated KPIs and ‘per unit’ benchmarks.

In the current climate with costs increasing, and the supply of new vehicles being constrained, one key measure which can give you an assessment of a dealer’s health in seconds is Overhead Absorption.

This KPI looks at the relationship between ‘non-sales direct profit’ and the fixed cost base. So let’s put that into English.

When we talk about ‘non-sales’ we look towards the aftersales income streams in the dealership.

In the simplest business model, this includes service and parts direct profit (being the operating profit after all of the department expenses have been deducted). Both departments normally deliver a consistent income stream to the business and are invaluable in balancing the business scales in a quieter sales month.

Indeed, when we consider aftersales, we should also look at other contributing departments.

Certainly, one of the industry shifts is towards a more diverse range of income streams, and with the impacts of the new car agency model still not fully known, we encourage many dealers to ensure they can control as much of the income entering their dealership directly, as they possibly can.

So, in future, we expect the non-sales income to also include

- Bodyshop and SMART repair

- Vehicle rental

- Vehicle valeting/detailing

- 'Destination’ income (think coffee concessions and EV charging hubs)

Anyhow, back to the KPI.

When you take all the aftersales income, we then look to compare this to the fixed (or overhead) cost base of the dealership. In this world where many dealers group exist in the UK, care does need to be taken to compare like with like, and certainly some level of caution does need to be applied where a dealership has a management charge levied on it.

The next part might bring anyone who hated maths at school into a cold sweat……

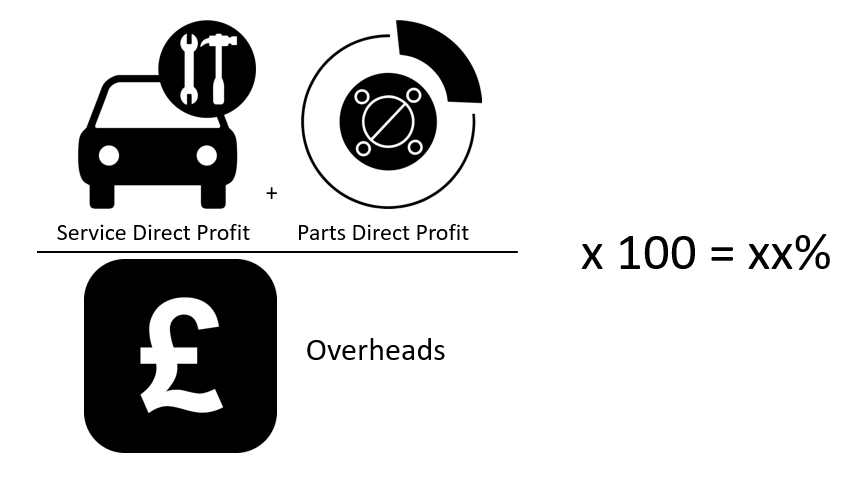

Non-Sales Direct Profit divided by Overheads expressed as a percentage.

In a dealership where the year to date direct profit from service is £200k and £100k from parts, and who has an overheads cost of £400k for the same period, this would mean:

- Non sales direct profit: £300k

- Overheads: £400k

- Overhead absorption: 75% (multiply the fraction above by 100)

Or expressed another way, the aftersales business ‘covers’ 75p in every £ of the overheads cost base. Meaning that to break even 25p needs to come from the sales departments, easier in a plate change month, but less certain when new car supply is problematic.

As a benchmark, many look towards the 80% threshold, but this is likely to come under pressure in the future months, although the recently announced support offered on heat and light costs will assist this in the short term.

Can it be over 100%? Absolutely! And where this is the case, it is usually down to a balance of tight cost control and an ‘on-target’ aftersales team.

For dealers, I think this is often one of those KPIs which most people nod about, but seldom stop to break it down, if this item assists one person in the motor retail industry, it’s been worth writing (and thanks for reading to this point).

The next step

For further information or support, please contact Ian McMahon or your usual UHY adviser.