30 January 2020

Within the 2019 Academies Financial Handbook (AFH) effective from 1 September 2019, the ESFA have significantly increased their guidance and focus on internal scrutiny for the 2019-20 year.

The detail is covered in Part 3 of the AFH, and to support these changes the ESFA have published an internal scrutiny best practice guide which we recommend you read.

The requirements for audit committees

First of all, it is worth a reminder than any academy trusts with annual income of over £50 million must have a dedicated audit committee; smaller trusts must either have a dedicated audit committee or can combine it with another committee (often the finance or resources committee). Larger multi-academy trusts (MATs) which fall below the £50 million threshold and therefore do not technically need a separate audit committee may, nevertheless, find that it is more practical to have one.

The role of an audit committee involves reviewing controls, safeguards, systems and procedures. Planning is required around the oversight of these functions and the role, especially for a sizeable MAT, can be time-consuming. A finance committee also has a demanding role overseeing financial performance and budgets, and combining the two committees may result in very long meetings, or the audit committee functions being relegated to second place.

Some key elements of Part 3 of the AFH are included here (and for ease of use, the term ‘audit committee’ is used throughout):

Key point - AFH 3.8

The audit committee’s role must include directing the trust’s programme of internal scrutiny and reporting to the board on the adequacy of the trust’s financial and other controls and management of risks.

Whilst an external audit firm, to whom internal audit services may be outsourced, can assist you with making your decision, and we have provided a document setting out example topics that you may wish to cover, it is the responsibility of the committee to set the programme of risk in response to the risk assessment.

Trusts may need to adopt different approaches and engage a range of professionals to complete work in a number of areas, including non-financial.

Key point – AFH 3.12 (extracts)

The committee must:

- have written terms of reference describing its remit

- agree a programme of work annually to deliver internal scrutiny that provides coverage across the year

- review the risk register to inform the programme of work, ensuring checks are modified as appropriate each year

- consider reports at each meeting from those carrying out the programme of work

- consider progress in addressing recommendations

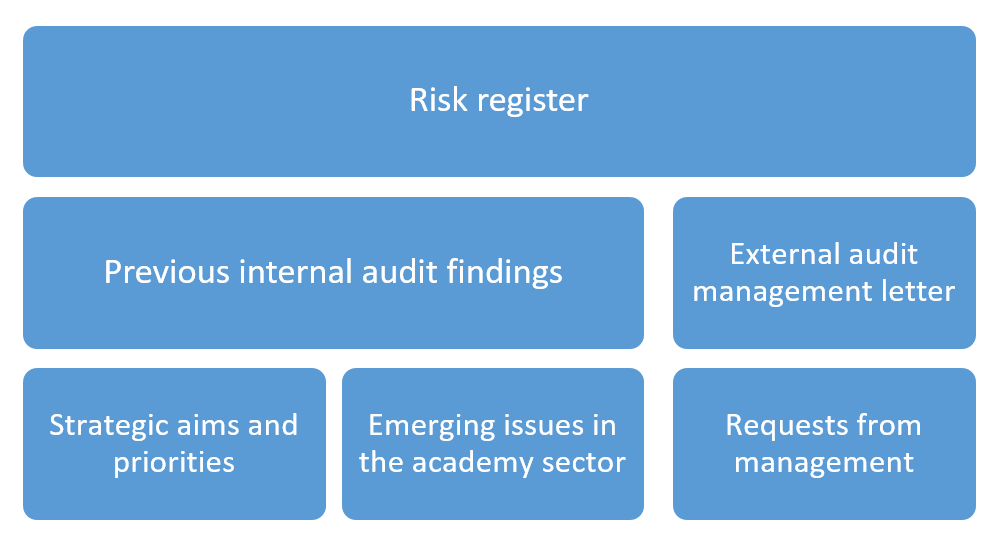

This means that the programme of internal scrutiny should link clearly from the risks highlighted on the risk register.

Whilst the risk register should be the driver to inform the programme of work, there are a number of sources of information that should be considered when determining an appropriate programme of assurance checks:

Key point –AFH 3.13

In MATs, the committee’s oversight must extend to the financial and other controls and risks at constituent academies.

Key point –AFH 3.14

Oversight must ensure information submitted to DfE and ESFA that affects funding, including pupil number returns and funding claims (for both revenue and capital grants) completed by the trust, and (for MATs) by constituent academies, is accurate and in compliance with funding criteria.

Key point – part of AFH 3.15 and 3.22

It is necessary to produce a short annual summary report to the audit committee for each year ended 31 August outlining the areas reviewed, key findings, recommendations and conclusions, to help the committee consider actions and assess year-on-year progress.

The trust must submit its annual summary report of the areas reviewed, key findings, recommendations and conclusions to ESFA by 31 December each year when it submits its audited annual accounts.

Key point – AFH 3.20

The trust must keep its approach to internal scrutiny under review. If it changes in size, complexity or risk profile, it should consider whether its approach remains suitable.

At the time of writing in mid-January, we are already well into month five of the 2019-20 financial year. If the programme of internal scrutiny work has not been set, then trusts need to urgently review their position to ensure a suitable programme can be delivered in the remainder of the year.

UHY provide internal audit services to a significant number of academy trusts. The following is a list of some of the themes or areas that we are commonly asked to review:

- Payroll and HR

- Procurement and value for money

- Governance, including AFH compliance

- Monthly financial closedown

- Fraud, theft and bribery

- Data and information security

- Fixed assets and capital income accounting

- Budgetary control and accuracy of management accounting information

- Pupil number returns

- Risk Management

- VAT

- Senior executive remuneration

If you have any questions then please do not hesitate to contact one of our academy experts.

Alternatively, fill out our Contact Form here.