A couple of weeks ago our Institute, ICAEW, published a tax infographic named “Tax Race: 54 years in the making”. It shows the breakdown of UK tax take between 1965 and 2019 by type of tax, and is interesting in a number of respects.

Today’s topic, though, is inheritance tax and the graphic shows a consistent position over those 54 years of inheritance tax being very much the poor relation, jostling with capital gains tax for bottom position throughout.

However, the tax has been on the increase of late, the ICAEW chart showing:

Year Tax Take

1995 £1.46bn

2000 £2.29bn

2005 £3.24bn

2010 £2.68bn

2015 £4.59bn

2019 £5.16bn

That increase in tax take since 2010 coincides with the nil rate band (the tax free allowance for inheritance tax) being frozen at £325,000 for a decade from 2010 until 2020. In his last budget speech, Chancellor Rishi Sunak announced that part of the payment for COVID support measures would be met by a further freezing of the allowance until 2025 meaning there will have been 15 years with no increase in the valuable allowance.

With house prices continuing to perform well, it doesn’t take rocket science to work out that more and more people are going to end up paying inheritance tax as a result of that freeze.

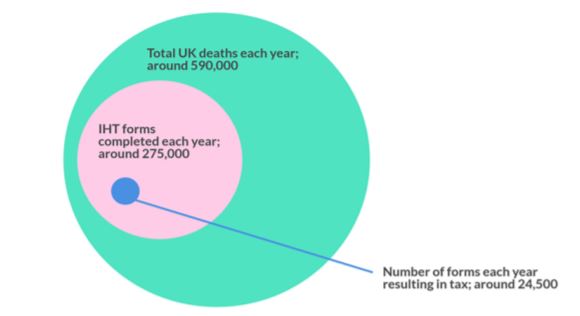

In July 2019, the Office of Tax Simplification published a report on inheritance tax which detailed the number of deaths, inheritance tax forms filed, and proportion of those resulting in tax paid (2015/16 tax year).

Source: Inheritance tax review - second report

This data shows that less than 10% of inheritance tax forms filed resulted in tax being paid, leading to the question, when is an inheritance tax return required to be filed?

The answer is framed negatively, a return being required unless one of the exemptions within the “Inheritance Tax (Delivery of Accounts)(Excepted Estates) Regulations 2011” removes that requirement. The three categories are:

- Low value estates:

- The deceased is domiciled within the UK

- Gross value of the estate and any chargeable gifts < £1,000,000

- No more than £150,000 of assets are held in trust

- No more than £100,000 of assets are overseas

- There are no lifetime chargeable transfers of value greater than £150,000

- There is no gift with reservation of benefit.

- Exempt estates:

- The deceased in domiciled within the UK

- Gross value of the estate and any chargeable gifts <£1,000,000

- Either spouse/civil partner or charity relief applies, with the chargeable value relief <£325,000

- Conditions c-f above apply

- Foreign domiciled estates:

- Deceased is non UK domiciled (and has never been actually or deemed UK domiciled)

- Value of the UK estate is entirely cash or quoted shares

- Gross value of these < £150,000

Many of these financial thresholds have not changed since 2006, whilst those tied to the nil rate band have stagnated alongside the nil rate band freeze.

Where a grant of probate is required, for example in order to sell or transfer a property or because a bank or investment holder requires one, but these criteria for an inheritance tax return are not met it is possible to use a simplified form IHT205 instead of the inheritance tax return IHT400.

With more and more inheritance tax being paid and with asset values outrunning frozen tax free allowances the taking of inheritance tax planning advice is becoming more relevant to more of the population. And with more and more estates falling outside of the excepted estates definition there is also a growing need for the taking of inheritance tax or probate advice following a death.

The next step

A number of UHY’s offices are regulated to carry out probate work and are able to offer holistic advice which encompasses inheritance tax and the wider tax position of the family of the deceased. To find out more please contact your usual UHY probate adviser.