Additional bonuses were available for those dealers willing to make the investment in solus and the concept of competing brands under the same manufacturer occupying the same building (eg. Seat and Skoda) was seen as the wrong thing to do to help develop growth in market share.

Fast forward five years, and the beginnings of change were starting to evidence themselves. Most notably JLR with their exciting (albeit high investment) Arch Concept and a general acceptance amongst many brands that costs needed to be taken out of the distribution channel in an increasingly online world.

Then the pandemic hit and the focus from both manufacturer and dealers has turned towards accelerating strategic change, especially given the enforced proof of concept of many of the digital changes that auto retailers saw coming down the line in the medium term. Many manufacturers have lost money through the pandemic period (the dealers less so) and naturally cost reduction is a focus. The temptation to rationalise networks, both in absolute size and by sharing facilities, is a tempting one and we are aware of changes that are planned or in progress with a number of brands in the UK.

On the 19th May, Stellantis (the newly formed merger between PSA and FCA and representing Peugeot, Citroen, DS, Vauxhall, Fiat, Alfa, Abarth and Jeep in the UK) announced a Europe wide restructure of their dealer network, commencing with the issue of termination notices for the two year rolling franchise agreement. Many dealers now face an uncertain few months awaiting the outcome of the new arrangements which will be outlined in July 2021.

So, what are we to expect?

PSA have made no secret of their desire to embrace multi-franchising in recent years, and this is particularly relevant within the Vauxhall dealerships which in many cases were designed for a significantly higher market share than that currently enjoyed. Likewise, FCA have been pushing multi-franchise for a number of years now under their Brand Centre concept. It seems inevitable that following the merger, the new group will seek to take advantage of the potential cost savings these arrangements offer by bringing the potential for all brands to come together.

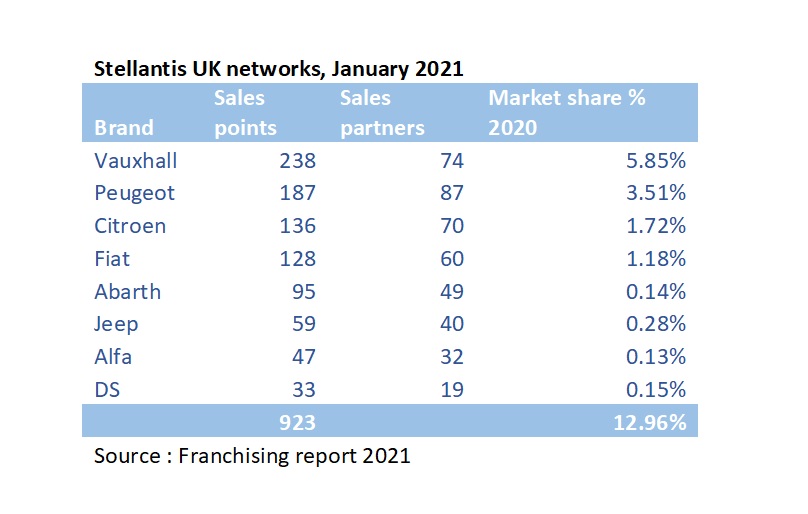

Another critical aspect we foresee is a rationalisation of the number of partners to help streamline the running of the National Sales Company. The table above shows the number of dealer partners and there will inevitably be scope to reduce this following the merger.

Aside from cost benefits, there are clear positives from being able to present a customer with a stable of brands offering choice and an enjoyable retail experience for a consumer. National sales companies need to be structured to ensure this style of retailing is embraced rather than risk in-fighting and battles over for example whether a customer chooses a Citroen over a Fiat.

Overall, it seems the multi-franchising concept is here to stay and offers clear operational efficiencies as well as customer experience benefits.

The next steps

For further information or support, please contact Paul Daly or your usual UHY adviser.