19 February 2020

Within the 2019 Academies Financial Handbook (AFH), which came into effect on 1 September 2019, the ESFA have further increased their guidance and focus on internal scrutiny and have introduced more detailed information about how your trust must periodically check the suitability of, and level of compliance with, its internal controls. This is an area where we have found some trusts struggling to establish their approach, and sector feedback suggested to us that more guidance would be helpful. Having an effective audit committee is the central pillar in the oversight of this work. The handbook explains that your audit committee will need to direct the programme of internal scrutiny, and must consider any recommendations made by your internal auditor or by other individuals the trust appoints to carry out the checks.

Details of the new guidance is covered within Part 3 of the AFH and, to further support the changes made, the ESFA have published an internal scrutiny best practice guide.

Audit committee requirements

Firstly, it is worth acknowledging that any academy trusts with annual income of over £50 million are required to have a dedicated audit committee; smaller trusts are able to combine the audit committee with another committee (often the finance or resources committee). Larger multi-academy trusts (MATs) which are below the £50 million threshold, and are therefore not required to have a separate audit committee, may still find that it is beneficial to have one.

An important role of the audit committee involves reviewing controls, safeguards, systems and procedures. Planning is integral in achieving an oversight of these functions, which can be heavily time-consuming for large MATs. It is important to appreciate the role a finance committee has in overseeing financial performance and budgets when considering combining the two committees, as this may result in lengthy meetings or the audit committee taking a less prominent position.

Some of the key elements identified within Part 3 of the AFH are included here (and for ease of use, the term ‘audit committee’ is used throughout):

Point of interest – AFH 3.8 (extracts)

The role of the audit committee must include managing the trust’s programme of internal scrutiny and reporting to the board on the suitability of the academy's financial and other controls and management of risks.

It is the responsibility of the audit committee to set the programme of risk management in response to the risk assessment. External auditors may be able to assist in identifying specific risk areas to target (a list of potential areas to consider is outlined at the end of this document).

Trusts may need to consider engaging a variety of specialists to complete the programmes of work, including non-financial.

Point of interest – AFH 3.12 (extracts)

The committee is required to:

- describe its remit in written terms

- agree a work programme annually to carry out internal scrutiny throughout the year

- ensure reports from those carrying out the work programme are reviewed at each meeting

- study progress in addressing recommendations that have been made

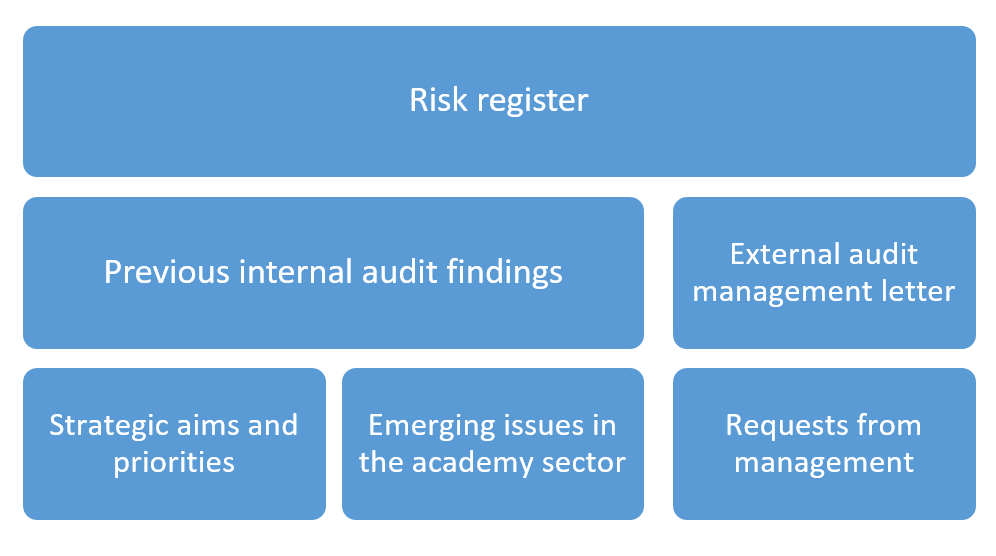

This means the programme of internal scrutiny should link clearly from the risks that are highlighted on the risk register. Ensuring risks are well managed has always been a key feature of the accountability framework for academy trusts, and your approach to internal scrutiny and the checks you make must be informed by the risks faced by the trust. For this reason, the handbook clarifies that you must maintain a risk register.

While the risk register should be the foundation for informing the work programme, there are a numerous sources of information that should be examined when assessing a suitable programme of assurance checks:

Point of interest – AFH 3.15 (extracts)

A short annual summary should be reported to the audit committee for each year which outlines the areas that have been reviewed, key findings, recommendations and conclusions in order to help the committee consider actions and assess progress made.

Point of interest – AFH 3.22

The trust is required to publish its annual summary report of the areas reviewed, key findings, recommendations and conclusions to the ESFA by 31 December each year, along with its audited annual accounts.

Point of interest – AFH 3.20

The trust is required to keep its approach to internal scrutiny under review, ensuring its approach remains appropriate in relation to any change in size or complexity.

Given that at the time of writing we are already well into the 2019-20 financial year, if the programme of internal scrutiny work has not yet been set, then trusts should immediately review the current position to ensure an appropriate programme can be delivered in the remainder of the year.

UHY provide internal audit services to a large number of academy trusts. The following is a list of some of the key areas that are we are often asked to review:

- Payroll and Human Resources

- Procurement and value for money

- Governance, including compliance with the AFH

- Monthly financial procedures

- Fraud, theft and bribery, including cash handling

- Data and information security, including GDPR compliance

- Fixed assets and oversight of the accounting of capital projects

- Management accounts information

- Risk Management

- VAT

- Senior leadership remuneration

If you have any questions then please do not hesitate to contact Ann Harrison on 0121 233 4799.