2 January 2020

UHY Hacker Young's Corporate Tax director, Nikhil Oza, explains some important tax considerations for self-employed professionals, as part of our Accounting for SMEs Q&A series.

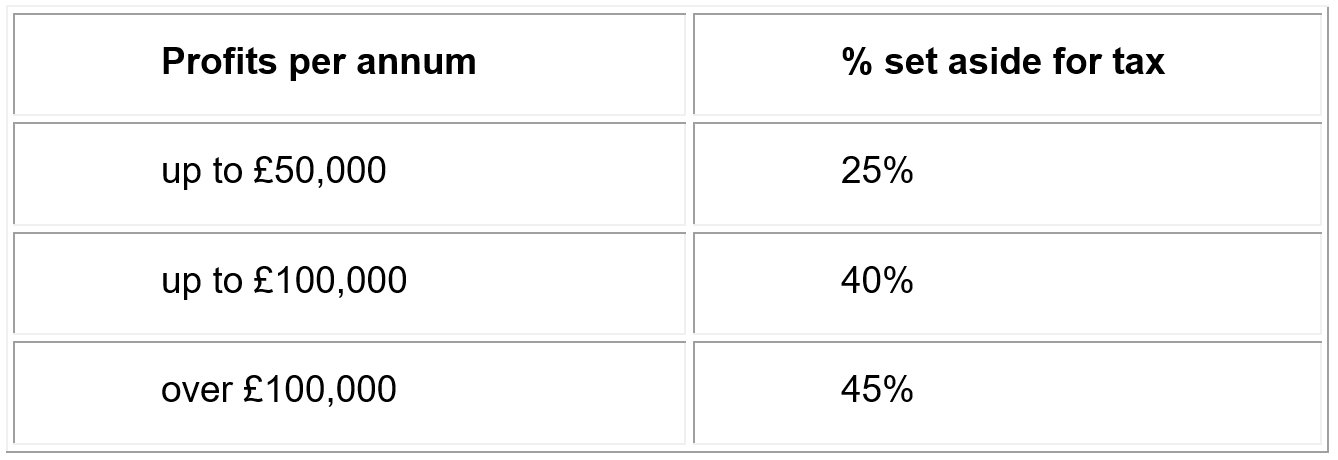

As a self-employed professional, how much of my income should I be putting aside for taxes?

As a self-employed individual, you are taxed on the profits that your business makes through your annual Self-Assessment tax return. Essentially, your taxable profit is the income that your business receives, minus the allowable business expenses incurred.

Obviously, the higher the amount of profit you report, the greater your tax liability will be. As a general guide, I would recommend you set aside the following amounts from your regular drawings to settle your Income Tax and National Insurance liabilities each year:

Remember, the above is only a guide and you may find that you need to set aside more if you have other sources of income.

How can self-employed professionals lower their tax burden? Are there any deductions that they should be aware of?

There are many ways that taxpayers can (legally) reduce their tax bill and each person’s circumstances will be different, so it is impossible to list them all! Speak to your accountant/tax adviser to ensure you have considered the below as a minimum:

- Make full use of tax-free allowances, such as the personal allowance, dividend allowance, savings allowance, marriage allowance, property and trading income allowance and annual CGT exempt amount to name but a few.

- The Rent-a-Room Relief, currently £7,500, where you let out a room in your home.

- Use your Individual Savings Account (ISA) entitlement to help you save tax-free.

- Pay into your pension pot to obtain tax relief.

- Give to charity - you will get tax relief if you are a higher-rate taxpayer.

- Don’t forget your SEIS/EIS investments provide income tax relief of up to 50%.

- Incorporation - one of the more advanced options, but setting up a company can yield tax savings given the corporation tax rate is only 19% (due to fall to 17% from 1 April 2020). There is an additional tax charge on getting money out of the company (usually by way of dividends) but the combined tax rate can still be lower than paying income tax rates of 40%/45%. Also, companies offer access to additional tax reliefs, such as Research and Development (R&D) Tax Relief (if the qualifying conditions are met) and can make inheritance tax planning easier. Download our R&D Tax Relief guide to find out more.

As a self-employed professional, what kind of financial records should I keep and how long do I need to keep them for (i.e. in case of an audit)?

You must keep your records for at least five years after the 31 January submission deadline of the relevant tax year. For example, if you sent your 2017-18 tax return online by 31 January 2019, you must keep your records until at least the end of January 2024.

HMRC may open an enquiry into your tax return and it is important to have complete records to show how you calculated your tax liability. They can charge a penalty if you fail to produce complete records when asked.

You’ll need to keep records/proof of:

- all sales and income (e.g. sales invoices, till rolls and bank slips)

- all business expenses (e.g. receipts and invoices for your purchases, goods and stock)

- bank statements and chequebook stubs

- VAT records if you’re registered for VAT

- PAYE records if you employ people

- records about your personal income

If you’re using traditional accounting (see our previous blog on the difference between traditional accounting and cash-basis accounting), you’ll also need to keep records of:

- what you’re owed but have not received yet

- what you’ve committed to spend but have not paid out yet, e.g. you’ve received an invoice but have not paid it yet

- the value of stock and work in progress at the end of your accounting period

- your year-end bank balances

- how much you’ve invested in the business in the year

- how much money you’ve taken out for your own use (i.e. your drawings)

There are no rules on how you must keep records. You can keep them on paper, digitally or as part of a software program (such as bookkeeping software). However, if you are subject to the Making Tax Digital requirements for VAT, then you would likely be keeping your records in a digital format. Your accountant should be able to take care of this for you if you wish.

What's next?

We will be posting the next in our Accounting for SMEs Q&A series shortly so watch this space! Our next piece will focus on important tax considerations for sole traders.

For more information on the issues mentioned above, or any other tax and accounting queries you may have, please contact Nikhil or your local UHY specialist.

Alternatively, fill out our contact form here.