3 April 2019

HMRC have proposed a dramatic change to how VAT is applied to construction services from 1 October 2019.

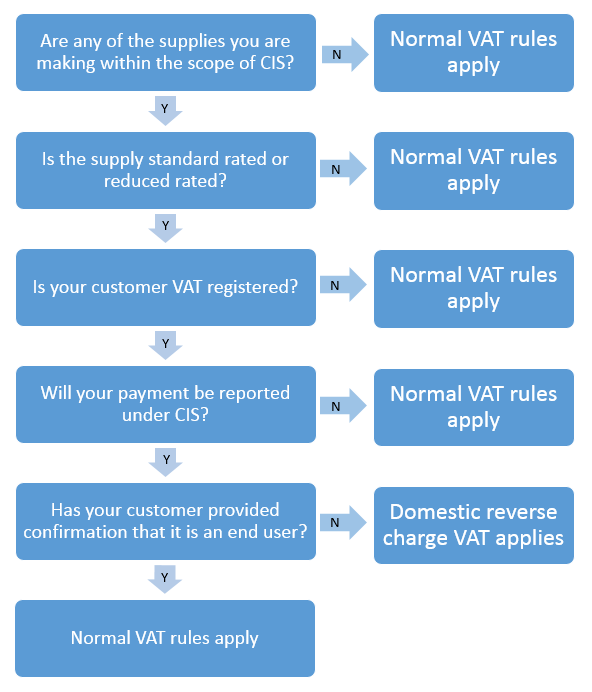

The domestic reverse charge ‘DRC’ will only affect supplies at the standard or reduced rates where payments are required to be reported through the Construction Industry Scheme ‘CIS’. The domestic reverse charge was first proposed and consulted on in 2017 and aims to combat missing trader fraud in the construction sector (similar to computer chips and mobile phones).

The DRC only applies where both the supplier and the customer are VAT registered, or required to be (note that supplies made under the DRC do not count towards the threshold) and it also only applies to supplies at the standard rate or reduced rate where payments are required to be reported through the Construction Industry Scheme ‘CIS’.

Therefore, supplies between sub-contractors and contractors, as defined by CIS, will be subject to the reverse charge unless they are supplied to a contractor who is an ‘end user’. In that regard it will not apply to where:

- Services are supplied to the end user, such as the property owner, or directly to a main contractor that sells a newly completed building to the customer

- The recipient makes onward supplies of those construction services to a connected company

- The supplier and recipient are landlord and tenant or vice versa, or

- The supplies are zero-rated.

The legislation has also been updated and now covers the supply of construction services that includes materials where it was previously believed to be just labour only.

Flowchart

Implementation

HMRC understands that this is a big shift in the rules and many businesses may have difficulties implementing them. HMRC on that basis will apply a ‘light touch’ in dealing with VAT errors in the first 6 months after introduction.

It is important to note that businesses that knowingly claim end user status when the DRC should have been applied will still be liable for the output tax that should have been paid and may also be subject to penalties.

End users?

End users are those who receive building and construction services but to not supply those services on along with other building and construction services. Many suppliers may not be aware that their customer is an end user, and it is up to the end user to make the supplier aware that they are an end user and that VAT should be charged in the normal way instead of under the DRC. We would recommend that suppliers get written confirmation from the end user of this fact.

Action points

- Review all contracts with regular suppliers to determine the exposure to the DRC

- Review your accounting systems so that supplies made under the DRC are entered correctly onto the VAT Return

- Consider the cash flow implications and put arrangements in place to ease any burden

If you have any queries regarding the domestic reverse charge, contact me or your local UHY adviser.