Publications that covered this story include The Sunday Times on 14 October 2018.

- Tax hike generates £808m in extra tax - 19% more than Government forecast

- Treasury benefitting from growing need for insurance to counter new business threats

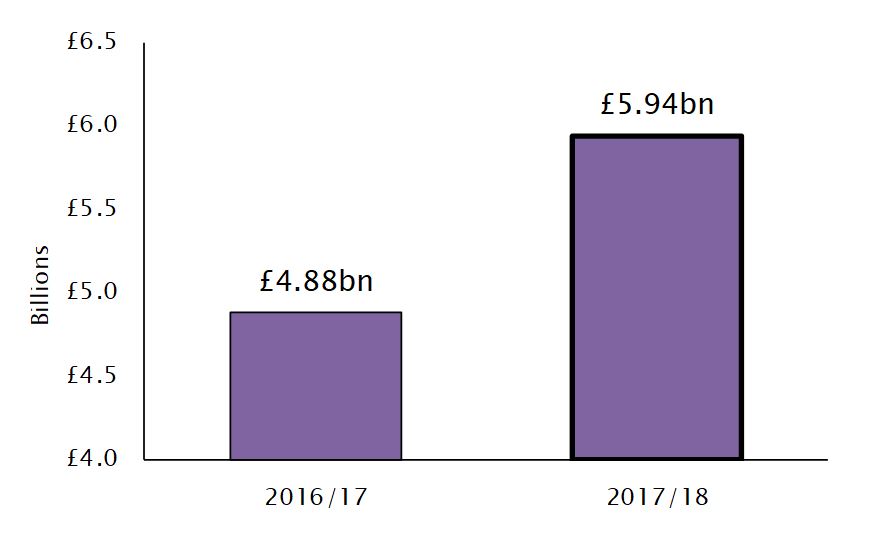

The Government’s income from Insurance Premium Tax increased to £6bn in 2017/18*, up 22% on £4.88bn collected the previous year – a far bigger impact on businesses and consumers than had been predicted by the Government, our research shows.

The Government increased the IPT rate from 10% to 12% in June last year, having announced it in the 2016 Autumn Budget. IPT is a tax on insurance policies that all insurance providers have to charge.

The Government forecast that the Insurance Premium Tax (IPT) increase would generate an extra £680m in tax raised. However, the added tax raised from businesses and consumers was £808m last year** - 19% more than the original prediction.

One of the key factors driving the higher than expected tax take is that businesses are having to take out more insurance policies than in the past. This has meant that – combined with the IPT increase itself – businesses are being hit twice.

While some policies such as employers’ liability insurance are compulsory, businesses are facing new threats that they have little choice but to insure against.

For example, businesses are having to insure against the growing threat of cybercrime. There were an estimated 1.7 million cybercrimes in the UK last year, but just 47 prosecutions related to computer hacking in 2017***. Businesses need to insure themselves against these risks as the Government has been unable to make a dent in the levels of cybercrime they face.

Recent research shows that nine out of ten UK businesses now have cyber insurance, up from just two in three a year ago****.

The income generated by Insurance Premium Tax has risen by 55% in two years, up from £3.8bn in 2015/16*.

Richard Lloyd-Warne, partner in our London office, says: “The Treasury is benefitting from the necessity of insurance by more than they had originally expected.”

“The fact is that businesses are now facing more threats than ever, all of which must be insured against. Just as the risk of a cyber-attack has ballooned over the last few years, new threats are likely to spring up in the future.”

“There are also a range of other insurance policies that many businesses are forced to buy such as employees’ liability insurance and professional indemnity.”

“The Government, however, could choose to concentrate taxation on areas that they want to discourage, rather than taxing something that businesses have little choice to do.”

Yield from Insurance Premium Tax reached £6bn in 2017/18, up 22% on the year before